VC: “Where’s the defensibility?”

Founder: “We have a great brand.”

Awkward silence…

I’m sure many a VC or Founder can relate to this exchange. VCs want to invest in companies that have network effects, strong lock in, or a competitive edge in technology or distribution. I have a sneaking suspicion, however, that today many VCs undervalue brands and place too high a premium on technology. I first began thinking about this because I noticed that more and more founders were alluding to “brand” during pitches. And given that founders are the best proxy for where opportunities lie, I thought it was worth paying attention to. USV’s recent thesis 3.0, which they recently published, made me more confident in this supposition.

I think there are three main reasons why brands are becoming an increasingly important component of high-growth technology businesses:

1.) The role of brands in society is evolving. More and more, consumers look to brands that align with their values and this emotional resonance breeds loyalty. Furthermore, in a world of massive informational overload — the average consumer is exposed to 3000 brands a day — trusted brands act as an effective heuristic for parsing through noise.

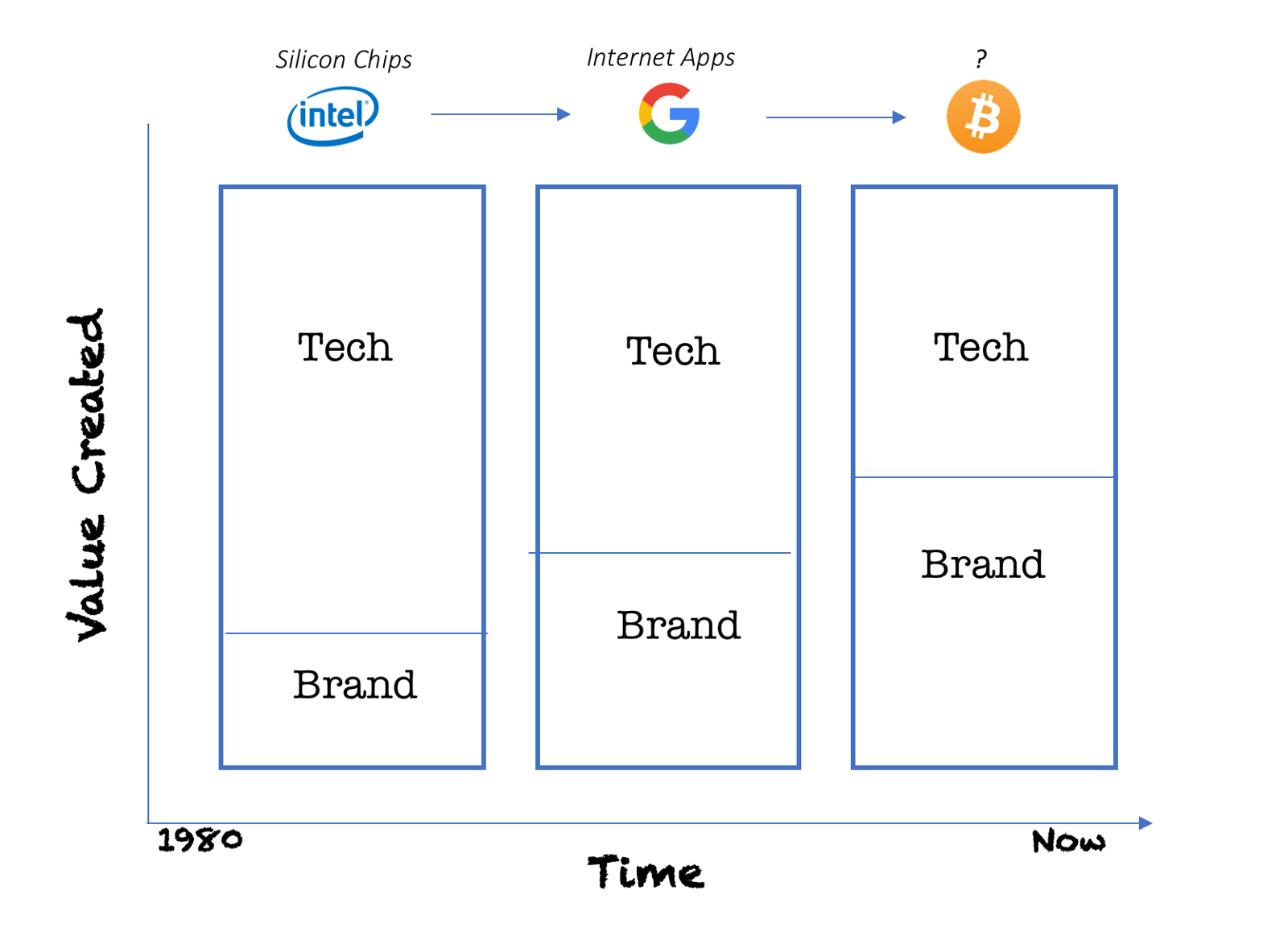

2.) The strength of technological moats has weakened due to the accelerated speed of innovation and the availability of global capital. Global VCs can fund proven business models at the drop of a hat and the major tech companies are constantly infringing on each other’s turf. Facebook copied Snapchat with ease, Amazon looms large over everyone, and Chinese and American bike-sharing companies duke it out with massive war chests. As Arjun Sethi wrote in this piece, the moat you have today simply grants you runway to create the next killer product. As these moats shrink, the distribution of value in the stack of a technology company shifts:

Indeed, as I sat down to write this over the weekend the merits of competitive moats were being debated by none other than Musk and Buffet. Buffet likes to invest in recognisable brands, such as Coca Cola, because of the moat they provide while Musk opined that moats are “lame” and companies should stay competitive through innovation. In this case, I think Musk is underestimating the moat that his personal brand has contributed to his companies.

3.) Distribution channels have opened up. The greatest challenge for a startup today, whether it’s a mattress company or a musical artist, is to foster awareness. Anyone can market a product through Instagram and distribute through Amazon but awareness and a loyal fan base, aka a brand, is invaluable. The theory of a long tail of winners has not manifested. We live in a blockbuster world: Kylie Jenner did $1BN in sales for her makeup line last year; Beyonce achieves goddess status; Tesla is overvalued because of Elon’s fan club; and WeWork justifies its sky high valuation with its “spirituality.”

Traditionally, VCs have not placed much value on “brand” because its value is intangible and difficult to quantify. The same goes for many public equities investors. But it’s clear from recent success stories, like Revolut and Robinhood, which achieved billion dollar valuations in record time that their nascent brands played an important role in their rapid growth. Indeed, Apple, perhaps the most recognised technology brand in the world, also happens to be the most valuable company in the world. Moving forward, investors and entrepreneurs will need to develop new mental models to better understand the role of brands in technology companies and early-stage startups. What exactly those mental models might be? Well, that’s for another post since I’m still figuring that part out!

If you enjoyed the post, please clap so others discover it. Cheers.